Herramientas de estabilización de los precios internos del azúcar en Colombia: ¿Funcionan?

DOI:

https://doi.org/10.17533/udea.le.n86a04Palabras clave:

Fondo de Estabilización de Precios del Azúcar, Sistema Andino de Franjas de Precios, cointegración, raíces unitarias, azúcar.Resumen

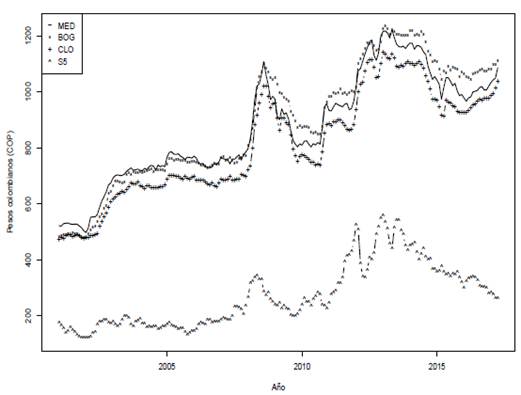

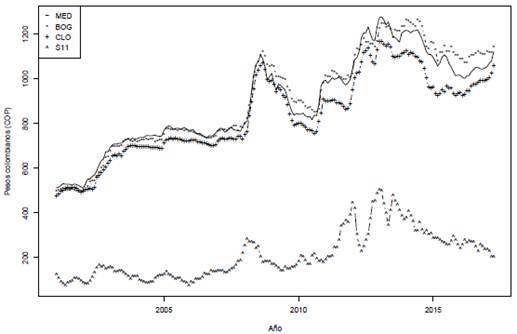

En 2001 entró en funcionamiento en Colombia el Fondo de Estabilización de Precios del Azúcar (FEPA) como un mecanismo para proteger a los productores locales de las fluctuaciones en los precios internacionales del azúcar, complementando al Sistema Andino de Franjas de Precios (SAFP) de la Comunidad Andina. Este trabajo busca establecer si el FEPA, unido al SAFP, ha aislado el precio local de las fluctuaciones en los precios del mercado internacional, para lo cual se determina si existe o no una relación de largo plazo entre los precios internacionales y sus contrapartes en las tres principales ciudades de Colombia. Utilizando una muestra para el periodo 2001-2015, no se pudo hallar evidencia de cointegración entre la serie de precios internacionales y los precios del azúcar en las ciudades estudiadas, pudiéndose concluir que el FEPA unido al SAFP ha tenido éxito aislando el efecto de los precios internacionales sobre los precios locales.

Descargas

Citas

Alonso, Julio César & Arcila, Andrés Mauricio (2013). “Empleo del comportamiento estacional para mejorar el pronóstico de un commodity: El caso del mercado internacional del azúcar”, Estudios Gerenciales, Vol. 29, No. 129, pp. 406-415. doi:10.1016/j.estger.2013.11.006.

Alonso, Julio César & Semaán, Paul (2010). “Prueba de HEGY en R”, apuntes de Economía, No. 23. Universidad ICESI, Colombia.

Arbeláez, María Angélica; Estacio, Alexander & Olivera, Mauricio (2010). “Impacto socioeconómico del sector azucarero colombiano en la economía nacional y regional”, Cuadernos de Fedesarrollo, No. 31. Fedesarrollo, Bogotá.

Breitung, Jörg (2002). “Nonparametric tests for unit roots and cointegration”, Journal of Econometrics, Vol. 108, No. 2, pp. 343-363. doi:10.1016/S0304-4076(01)00139-7.

Breusch, Trevor S. (1978). “Testing for Autocorrelation in Dynamic Linear Models”, Australian Economic Papers, Vol. 17, No. 31, pp. 334-355. doi:10.1111/j.1467-8454.1978.tb00635.x.

Bugueiro, Mauricio; Brümmer, Bernhard & Díaz, Jose (2010). “Market integration and price leadership in selected sugar markets. The case of Colombia, Brazil and the world”, Economía Agraria, Vol. 14, pp. 23-32.

Cashin, Paul; Liang, Hong & McDermott, C. John (2000). “How persistent are shocks to world commodity prices?”, IMF Staff Papers, Vol. 47, No. 2, pp. 177-217. doi:10.2307/3867658.

Clark, J. Stephen & Klein, K. Kurt (1994). “The Relationship Between Price Stabilization and Cycles in the Canadian Wheat Market”, Agricultural and Resource Economics Review, Vol. 23, No. 1, pp. 22-28.

Dickey, David A. & Fuller, Wayne A. (1979). “Distribution of the Estimators for Autoregressive Time Series With a Unit Root”, Journal of the American Statistical Association, Vol. 74, No. 366, pp. 427-431. doi:10.2307/2286348.

Engle, Robert F. (1982). “Autoregressive Conditional Heteroscedasticity with Estimates of the Variance of United Kingdom Inflation”, Econometrica, Vol. 50, No. 4, pp. 987-1007. doi:10.2307/1912773.

Ghysels, Eric; Lee, Hahn S. & Noh, Jaesum (1994). “Testing for unit roots in seasonal time series: some theoretical extensions and a Monte Carlo investigation”, Journal of Econometrics, Vol. 62, No. 2, pp. 415-442. doi:10.1016/0304-4076(94)90030-2.

Godfrey, Leslie G. (1978). “Testing Against General Autoregressive and Moving Average Error Models when the Regressors Include Lagged Dependent Variables”, Econometrica, Vol. 46, No. 6, pp. 1293-1301. doi:10.2307/1913829.

Hylleberg, Svend; Engle, Robert F.; Granger, Clive W. J. & Yoo, B. S. (1990). “Seasonal integration and cointegration”, Journal of Econometrics, Vol. 44, No. 1-2, pp. 215-238. doi:10.1016/0304-4076(90)90080-D.

Johansen, Søren (1991). “Estimation and Hypothesis Testing of Cointegration Vectors in Gaussian Vector Autoregressive Models”, Econometrica, Vol. 59, No. 6, pp. 1551-1580. doi:10.2307/2938278.

Kwiatkowski, Denis; Phillips, Peter C. B.; Schmidt, Peter & Shin, Yongcheol

(1992). “Testing the null hypothesis of stationarity against the alternative of a unit root”, Journal of Econometrics, Vol. 54, No. 1-3, pp. 159-178. doi:10.1016/0304-4076(92)90104-Y.

Massell, Benton F. (1969). “Price Stabilization and Welfare”, Quarterly Journal of Economics, Vol. 83, No. 2, pp. 284-298.

Miranda, Mario J. & Helmberger, Peter G. (1988). “The Effects of Commodity Price Stabilization Programs”, The American Economic Review, Vol. 78, No. 1, pp. 46-58.

Newbery, David M. & Stiglitz, Joseph E. (1979). “The theory of commodity price stabilisation rules: Welfare impacts and supply responses”, The Economic Journal, Vol. 89, No. 356, pp. 799-817.

Oi, Walter Y. (1961). “The Desirability of Price Instability Under Perfect Competition”, Econometrica: Journal of the Econometric Society, Vol. 29, No. 1, pp. 58-64.

Phillips, Peter C. B. & Ouliaris, Sam (1990). “Asymptotic Properties of Residual Based Tests for Cointegration”, Econometrica, Vol. 58, No. 1, pp. 165-193. doi:10.2307/2938339.

Phillips, Peter C. B. & Perron, Pierre (1988). “Testing for a unit root in time series regression”, Biometrika, Vol. 75, No. 2, pp. 335-346. doi:10.1093/biomet/75.2.335.

Prada, Tatiana (2004). “Análisis del Efecto en el Bienestar de la Incorporación del Fondo de Estabilización de Precios del Azúcar en Colombia”, Serie Documentos de Investigación, Vol. 158. Departamento de Economía y Administración, Universidad Alberto Hurtado.

R Core Team (2013). R: A language and environment for statistical computing. Vienna, Austria: Foundation for Statistical Computing.

Tudela, Juan Walter; Rosales, Ramón & Samacá, Henry (2004). “Un Análisis Empírico del Fondo de Estabilización de Precios en el Mercado de Aceite de Palma Colombiano”, Documentos CEDE, 2004/35. Universidad de los Andes, Colombia.

Waugh, Frederick V. (1944). “Does the Consumer Benefit from Price Instability?”, Quarterly Journal of Economics, Vol. 58, No. 4, pp. 602-614. doi: 10.2307/1884746.

Publicado

Cómo citar

Número

Sección

Licencia

Derechos de autor 2017 Julio César Alonso Cifuentes, Andrés Mauricio Arcila Vásquez, Sebastián Montenegro Arana

Esta obra está bajo una licencia internacional Creative Commons Atribución-NoComercial-CompartirIgual 4.0.

Este sitio web, por Universidad de Antioquia, está licenciado bajo una Creative Commons Attribution License.

Los autores que publiquen en esta revista aceptan que conservan los derechos de autor y ceden a la revista el derecho de la primera publicación, con el trabajo registrado con una Licencia de Atribución-NoComercial-CompartirIgual de Creative Commons, que permite a terceros utilizar lo publicado siempre que mencionen su autoría y a la publicación original en esta revista.

Los autores pueden realizar acuerdos contractuales independientes y adicionales para la distribución no exclusiva de la versión del trabajo publicada en la revista (por ejemplo, incluirla en un repositorio institucional o publicarla en un libro) siempre que sea con fines no comerciales y se reconozca de manera clara y explícita que el artículo ha sido originalmente publicado en esta revista.

Se permite y recomienda a los autores publicar sus artículos en Internet (por ejemplo, en páginas institucionales o personales), ya que puede conducir a intercambios provechosos y a una mayor difusión y citación de los trabajos publicados.