Prévisibilité de la bourse colombienne

DOI :

https://doi.org/10.17533/udea.le.n91a04Mots-clés :

prévisibilité, prime de risque, dividende de rendement, marché boursier colombien, retours attendusRésumé

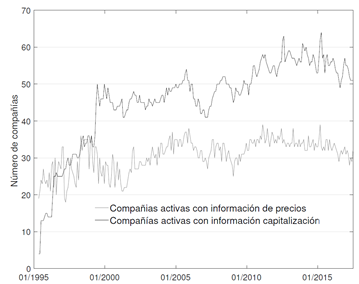

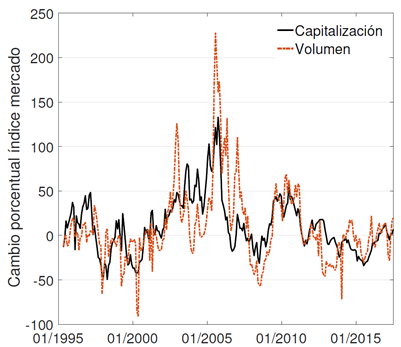

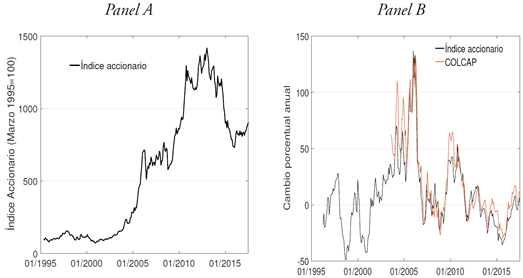

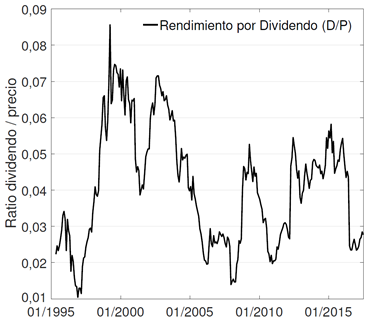

Cet article étudie les rendements historiques du marché boursier colombien et sa prévisibilité à moyen et long terme, afin de déterminer si la prime de risque est variable ou constante dans le temps et quelle est sa relation avec d’autres variables économiques. . Pour cela, un indice de prix, de rendements et de dividendes est construit pour la période 1995-2017, considérant l’ensemble des émetteurs des titres à revenus variables sur marché des actions en Colombie. Il est conclu que les fluctuations du rapport prix/dividende du marché boursier colombien s’expliquent principalement par les variations des rendements futurs, ce qui implique que le marché est soumis à des cycles et que la prime de risque est variable dans le temps. En outre, il a été constaté que les informations sur les prêts au logement, le taux de change réel et les rendements de l’indice S&P500 contribuaient à accroître le pouvoir de prévision...

Téléchargements

Références

Alonso, J. C. & García, J. (2009). ¿Qué tan buenos son los patrones del IGBC para predecir su comportamiento?: Una aplicación con datos de alta frecuencia. Estudios Gerenciales, 25(11),13-36.

Ang, A. & Bekaert, G. (2007). Stock return predictability: Is it there? The Review of Financial Studies, 20(3), 651-707.

Arango, L. E., González, A. & Posada, C. (2002). Returns and the interest rate: a non-linear relationship in the Bogotá stock market. Applied Financial Economics, 12(11), 835-842.

Bastidas, A. (2008). Incertidumbre de la prima de riesgo del mercado accionario de Colombia 1991-2007. Perfil de Coyuntura Económica, 12, 159–178.

Boyd, J., Hu, J. & Jagannathan, R. (2005). The Stock Market’s Reaction to Unemployment News: Why Bad News Is Usually Good for Stocks. The Journal of Finance, 60(2), 649–672.

Campbell, J. Y. & Ammer, J. (1993). What Moves the Stock and Bond Markets? A Variance Decomposition for Long-Term Asset Returns. The Journal of Finance, 48(1), 3–37.

Campbell, J. Y. (1987). Stock Returns and the Term Structure. Journal of Financial Economics, 18(2), 373–399.

Campbell, J. Y. (1990). Measuring the Persistence of Expected Returns (NBER working paper No. 3305). Recuperado del sitio web The National Bureau of Economic Research: https://www.nber.org/papers/w3305

Campbell, J. & Shiller, R. (1988a). The Dividend-Price Ratio and Expectations of Future Dividends and Discount Factors. The Review of Financial Studies, 1(3), 195–228.

Campbell, J. & Shiller, R. (1988b). Stock Prices, Earnings, and Expected Dividends. The Journal of Finance, 43(3), 661–676.

Chen, N.-F., Roll, R. & Ross, S.A. (1986). Economic Forces and the Stock Market. Journal of Business, 59(3), 383–403.

Cochrane, J. (2007). The Dog that Did Not Bark: A Defense of Return Predictability. The Review of Financial Studies, 21(4), 1533–1575.

Cochrane, J. (2011). Presidential Address: Discount Rates. The Journal of Finance, 66 (4), 1047-1108.

Cutler, D., Poterba, J. & Summers, L. H. (1989). What Moves Stock Prices? Journal of Portfolio Management, 15(2), 4-12.

Fama, E. F. (1981). Stock Returns, Real Activity, Inflation, and Money. The American Economic Review, 71(4), 545-565.

Fama, E. F. & Schwert, G. (1977). Asset returns and inflation. Journal of Financial Economics, 5(2), 115–146.

Geske, R. & Roll, R. (1983). The Fiscal and Monetary Linkage between Stock Returns and Inflation. The Journal of Finance, 38(1), 1–33.

Gómez-Sánchez, A.M. & Astaiza-Gómez, J. (2015). Primas de riesgo de renta variable ex-post y ciclos económicos en Colombia: Una investigación empírica utilizando los filtros de Kalman y Hodrick-Prescott. Revista Finanzas y Política Económica, 7 (1), 109-129.

Goyal, A. & Welch, I. (2003). Predicting the Equity Premium with Dividend Ratios. Management Science, 49(5), 639–654.

Harvey, C. (1991). The World Price of Covariance Risk. The Journal of Finance, 46 (1), 111–157.

Hjalmarsson, E. (2010). Predicting Global Stock Returns. Journal of Financial and Quantitative Analysis, 45(1), 49–80.

Kristjanpoller, W. & Muñoz, R. (2012). Analysis of Day of the Week Effect in the main Latin-American stock markets: an approximation through the Stochastic Dominance Criterion. Estudios de Economía, 39(1), 5-26.

Larrain, B. & Yogo, M. (2008). Does firm value move too much to be justified by subsequent changes in cash flow? Journal of Financial Economics, 87 (1), 200–226.

Lettau, M. & Ludvigson, S. (2005). Expected returns and expected dividend growth. Journal of Financial Economics, 76 (3), 583–626.

Lo, A. W. & MacKinlay, A. (1988). Stock Market Prices do not Follow Random Walks: Evidence from a Simple Specification Test. The Review of Financial Studies, 1(1), 41–66.

Ludvigson, S. C. & Ng, S. (2009). Macro Factors in Bond Risk Premia. The Review of Financial Studies, 22(12), 5027-5067.

Montenegro, A. (2007). El efecto día en la bolsa de valores de Colombia (Documentos de Economía No. 2007-09). Recuperado del Departamento de Economía, Pontificia Universidad Javeriana, Bogota.

Nelson, C. R. (1976). Inflation and Rates of Return on Common Stocks. The Journal of Finance, 31(2), 471–483.

Newey, W. & West, K. (1987). A Simple, Positive Semi-Definite, Heteroskedasticity and Autocorrelation Consistent Covariance Matrix. Econometrica, 55(3), 703–708.

Ochoa, C. M. & Avendaño, G. I. (2005). The Unification of the Colombian Stock Market: A Step Towards Efficiency–Empirical Evidence. Latin American Business Review, 5(4), 69–98.

Ospina, J. (2007). Características generales del mercado accionario colombiano como mercado emergente. Economía y Desarrollo, 6 (1), 105-136.

Pearce, D. & Roley, V. (1983). The Reaction of Stock Prices to Unanticipated Changes in Money: A note. The Journal of Finance, 38(4), 1323–1333.

Perez-Villalobos, J. & Mendoza-Gutiérrez, J. (2010). Efecto día en el mercado accionario colombiano: una aproximación no paramétrica (Borradores de Economía, No. 585). Recuperado del Banco de la República: http://www.banrep.gov.co/es/borrador-585

Rangvid, J., Schmeling, M. & Schrimpf, A. (2014). Dividend Predictability Around the World. Journal of Financial & Quantitative Analysis, 49(5-6), 1255–1277.

Rapach, D., Strauss, J. & Zhou, G. (2013). International Stock Return Predictability: What Is the Role of the United States? The Journal of Finance, 68(4), 1633-1662.

Rapach, D., Wohar, M. & Rangvid, J. (2005). Macro variables and international stock return predictability. International Journal of Forecasting, 21(1), 137–166.

Restrepo, M., Zuluaga, S. & Guerra, M. (2002). El mercado de capitales colombiano en los noventa y las firmas comisionistas de bolsa. Colección Economía Colombiana. Bogotá. Fedesarrollo.

Sierra, K., Duarte, J. & Ortiz, V. (2015). Predictibilidad de los retornos en el mercado de Colombia e hipótesis de mercado adaptativo. Estudios Gerenciales, 31(137), 411–418.

Solnik, B. (1993). The performance of international asset allocation strategies using conditioning information. Journal of Empirical Finance, 1(1), 33–55.

Vélez-Pareja, I. (2000). The Colombian Stock Market: 1930-1998. Latin American Business Review, 1(4), 61–84.

Yepes-Rios, B., Gonzalez-Tapia, K. & Gonzalez-Perez, M. (2015). The integration of stock exchanges: The case of the Latin American Integrated Market (MILA) and its impact on ownership and internationalization status in Colombian brokerage firms. Journal of Economics, Finance and Administrative Science, 20(39), 84–93.

Téléchargements

Publié-e

Comment citer

Numéro

Rubrique

Licence

(c) Tous droits réservés José Ignacio López-Gaviria 2019

Cette œuvre est sous licence Creative Commons Attribution - Pas d'Utilisation Commerciale - Partage dans les Mêmes Conditions 4.0 International.

Cette page, par Universidad de Antioquia, est autorisée sous une Licence d'attribution Creative Commons.

Les auteurs qui publient avec cette revue acceptent de conserver les droits d'auteur et d'accorder le droit de première publication à la revue, l'article sous licence sous une licence Creative Commons Attribution-NonCommercial-ShareAlike permettant à d'autres de le partager tant qu'ils reconnaissent sa paternité et sa publication originale dans ce journal.

Les auteurs peuvent conclure des accords contractuels supplémentaires et distincts pour la distribution non exclusive de la version publiée de la revue (par exemple, la publier dans un référentiel institutionnel ou la publier dans un livre), à condition que ces accords soient sans but lucratif et être reconnu comme la source originale de publication.

Les auteurs sont autorisés et encouragés à publier leurs articles en ligne (par exemple, dans des dépôts institutionnels ou sur leurs sites Web), car cela peut conduire à de précieux échanges ainsi qu'à une plus grande citation des travaux publiés.

tenemos que ρ ≈ 0; 99, que es consistente con un rendimiento por dividendo mensual de 0,34 %. A partir de la aproximación de primer orden, el logaritmo de los retornos se define como:

tenemos que ρ ≈ 0; 99, que es consistente con un rendimiento por dividendo mensual de 0,34 %. A partir de la aproximación de primer orden, el logaritmo de los retornos se define como:

. De la ecuación anterior (omitiendo los gorros), podemos escribir el (log) rendimiento por dividendo como la resta de los retornos y el crecimiento de los dividendos más el valor (descontando) del rendimiento por dividendo del siguiente período:

. De la ecuación anterior (omitiendo los gorros), podemos escribir el (log) rendimiento por dividendo como la resta de los retornos y el crecimiento de los dividendos más el valor (descontando) del rendimiento por dividendo del siguiente período:

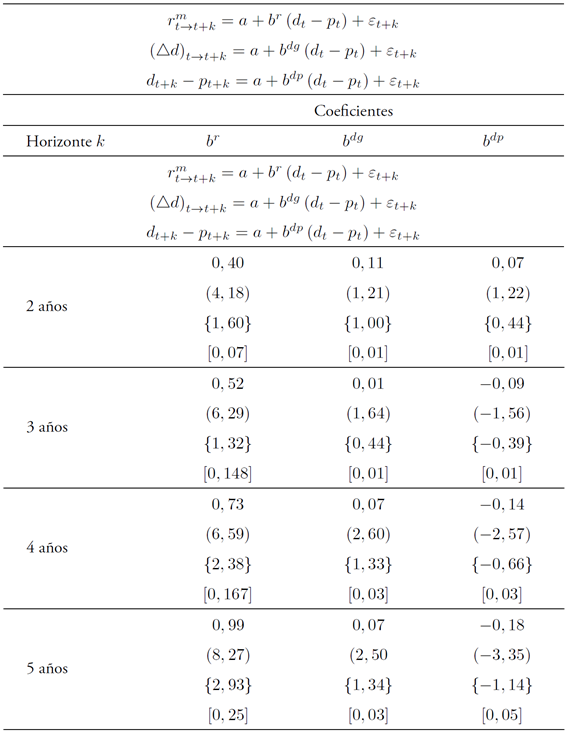

es el logaritmo del retorno mensual acumulado entre cada período y un horizonte (, descontado del promedio.

dt ( pt

es el logaritmo del rendimiento por dividendo descontando del promedio.

es el logaritmo del retorno mensual acumulado entre cada período y un horizonte (, descontado del promedio.

dt ( pt

es el logaritmo del rendimiento por dividendo descontando del promedio.  es la tasa de crecimiento de dividendos acumulado entre cada período y el horizonte (: Todos los datos son mensuales para el período abril 1995 - julio 2017. El estadístico t es reportado entre paréntesis. Entre llaves está reportado el t-estadístico bajo errores estándar corregidos por autocorrelación y heterocedasticidad (

es la tasa de crecimiento de dividendos acumulado entre cada período y el horizonte (: Todos los datos son mensuales para el período abril 1995 - julio 2017. El estadístico t es reportado entre paréntesis. Entre llaves está reportado el t-estadístico bajo errores estándar corregidos por autocorrelación y heterocedasticidad (

es el logaritmo del retorno mensual acumulado entre cada período y un horizonte ( descontado del promedio.

dt ( pt

es el logaritmo del rendimiento por dividendo descontando del promedio. Los datos corresponden a observaciones mensuales para el período abril 1995-julio 2017. La significancia estadística de los coeficientes está indicada por *, donde p<0,001***, p<0,05** y p<0,1*.

es el logaritmo del retorno mensual acumulado entre cada período y un horizonte ( descontado del promedio.

dt ( pt

es el logaritmo del rendimiento por dividendo descontando del promedio. Los datos corresponden a observaciones mensuales para el período abril 1995-julio 2017. La significancia estadística de los coeficientes está indicada por *, donde p<0,001***, p<0,05** y p<0,1*.